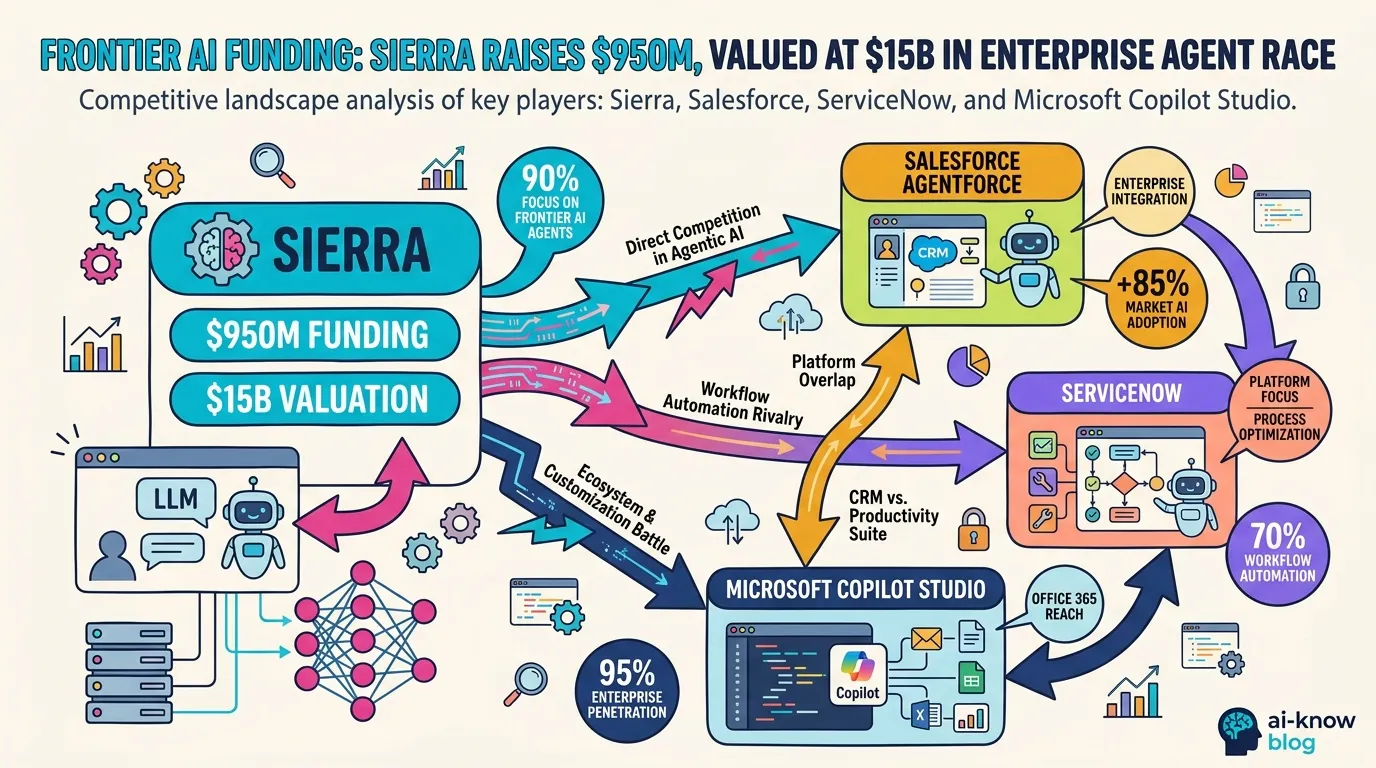

Sierra's $950M Raise Signals the Enterprise AI Consolidation War

With a $15B+ valuation, native AI startups and legacy CRM giants are now in direct competition

Bret Taylor — former co-CEO of Salesforce and former OpenAI board chair — has closed a $950M financing round for Sierra, the enterprise AI agent startup he co-founded. Led by Tiger Global and GV (Google Ventures), the raise pushes Sierra’s post-money valuation north of $15 billion, roughly doubling its previous mark.

The headline number matters less than what it signals: the Enterprise AI market has crossed the threshold from “proof-of-concept” into full-scale competitive warfare.

Sierra’s Edge: The Pure-Play Agent Advantage

Sierra sells conversational AI agents that handle enterprise customer interactions — with deep inroads into retail, telecom, and insurance. As an Agentic AI-native startup, Sierra’s clearest advantage is architectural freedom. Unlike Salesforce or ServiceNow, Sierra carries no decades of technical debt and can build around the latest frontier models from scratch.

Taylor’s CRM insider knowledge amplifies this. He can embed industry-specific compliance requirements into the initial product design — something legacy players retrofitting AI onto existing stacks find genuinely difficult to replicate.

Where the $950M Goes

The funding is earmarked primarily for expanded access to frontier models and the development of vertical-specific fine-tuning pipelines and data infrastructure.

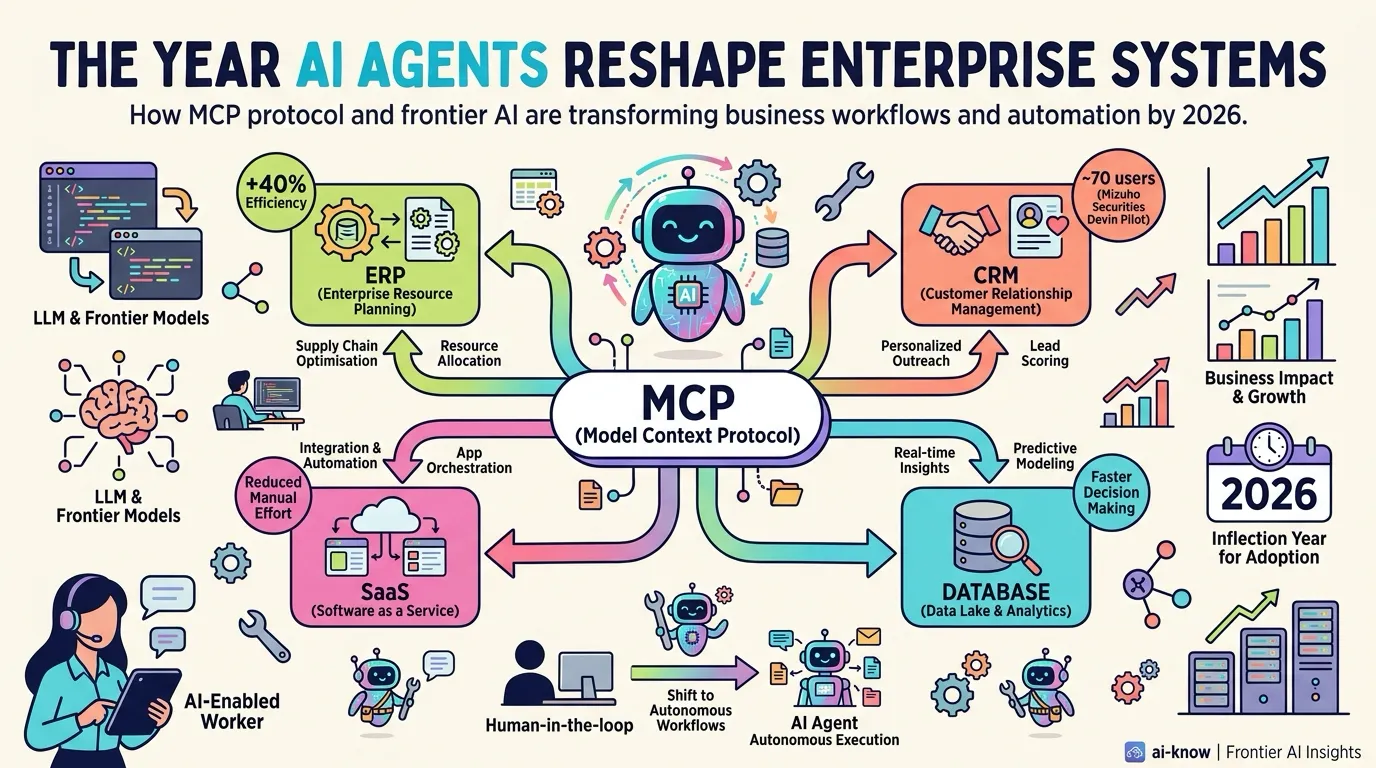

The more interesting strategic signal is the multi-model architecture approach. Rather than tying to a single model provider, Sierra intends to route tasks to the best-fit model dynamically. This pattern is rapidly becoming the new frontier of AI Commercialization. For highly regulated industries like insurance and telecom, industry-specific fine-tuning doubles as a competitive moat: it is the kind of compounding advantage that incumbents find difficult to replicate late.

The Lab vs. Tool Split Is Now Defined

Enterprise AI in 2026 has crystallized into two camps.

“The next battle isn’t about model capability — it’s about who has the deeper industry data and trust relationships.”

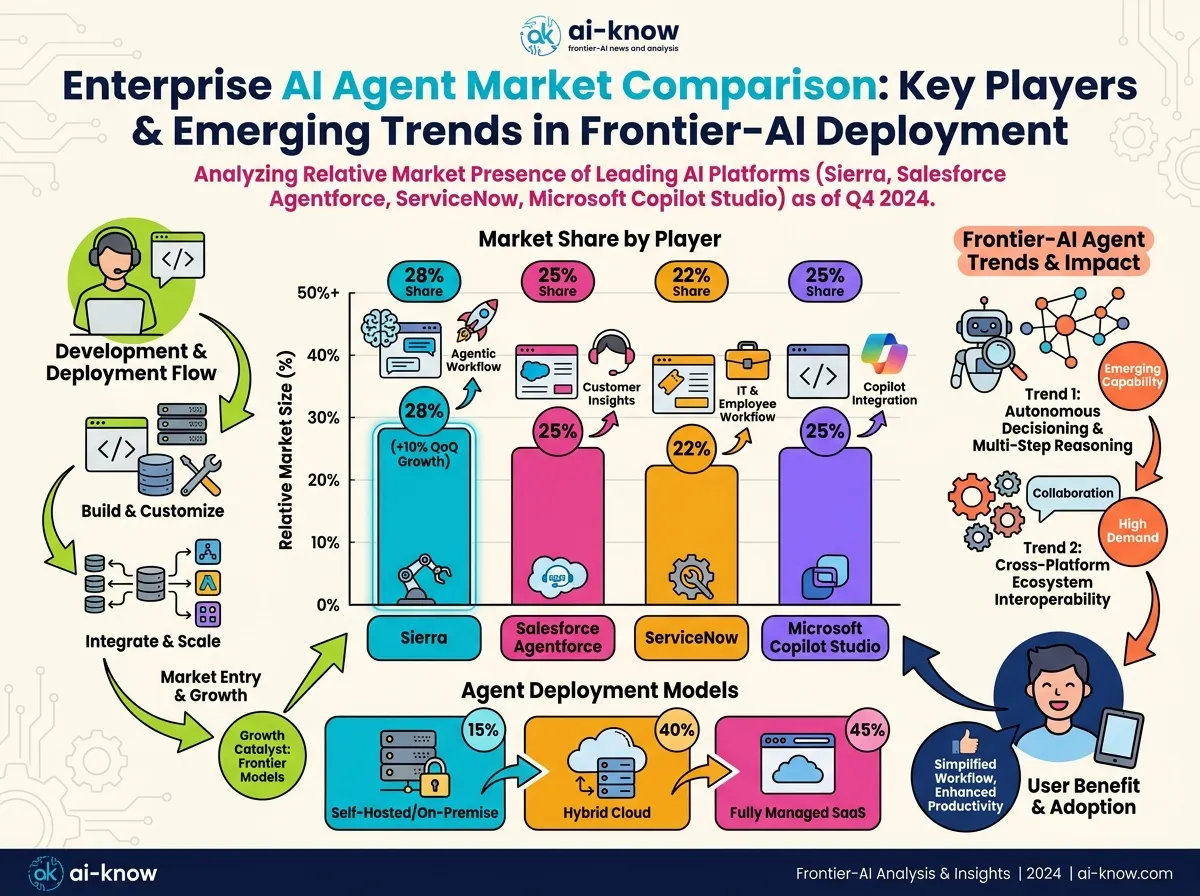

Lab-side (Anthropic Claude for Enterprise, OpenAI Workspace Agents): delivers frontier-model capability directly to enterprise buyers. Tool-side (Sierra, Salesforce Agentforce, ServiceNow, Microsoft Copilot Studio): provides the “plumbing” that plugs AI agents into existing business workflows.

Sierra occupies the purest “agent-only” position on the tool side. Where Salesforce leans on its existing CRM installed base, Sierra competes horizontally across industries — a riskier bet, but one that avoids single-market concentration risk.

What Enterprises Should Take Away

Three practical takeaways for enterprise buyers:

First, avoid early single-vendor lock-in. With competitors still jockeying for position, preserving multi-vendor optionality is worth the overhead.

Second, your proprietary vertical data is the next moat. Sierra’s bet on industry-specific fine-tuning reflects a broader truth: who controls the domain data will control the agent layer in two to three years.

Third, your existing CRM/ERP vendor contracts deserve a fresh look. As Salesforce and ServiceNow accelerate their agent features, benchmarking them against native AI startups has become a legitimate exercise.

Sources: Sierra raises $950M as the race to own enterprise AI gets serious — TechCrunch AI, 2026

Related Articles

Anthropic Launches Claude for Small Business: 15 Agentic Workflows to Close the SMB AI Gap

Anthropic and OpenAI Race to Form Enterprise AI Joint Ventures

Anthropic Launches "Code w/ Claude 2026" — The Next Chapter of Agentic Coding Begins in SF

ServiceNow's AI Control Tower: Agentic AI Governance from Desktops to Data Centers

Accenture × NSK: AI-Driven Business Reinvention Moves to Full Scale in Japanese Manufacturing