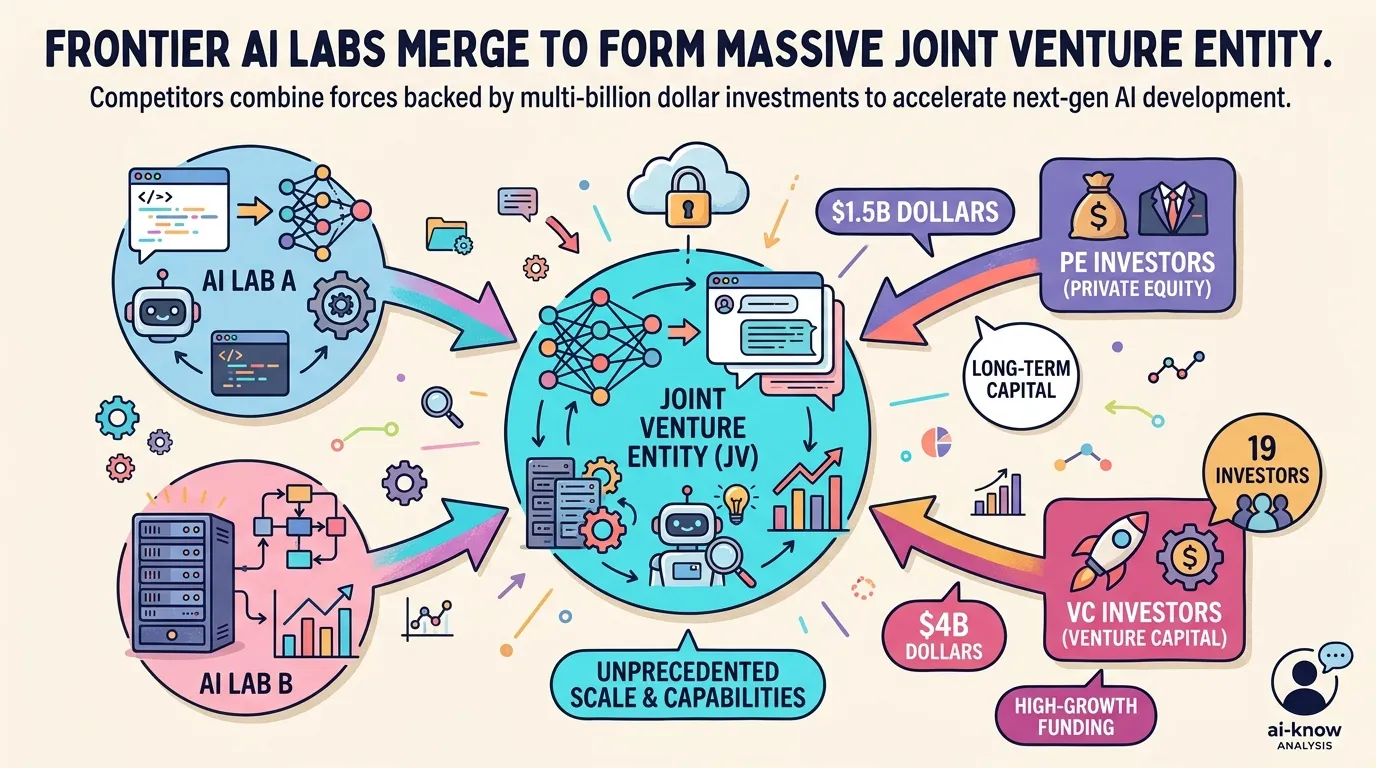

Anthropic Launches $1.5B Enterprise AI Services Joint Venture with Blackstone and Goldman Sachs

Forward-deployed engineers, PE portfolio pipelines, and a Palantir-style implementation model — Anthropic is going after the consulting market directly, and OpenAI is reportedly right behind it

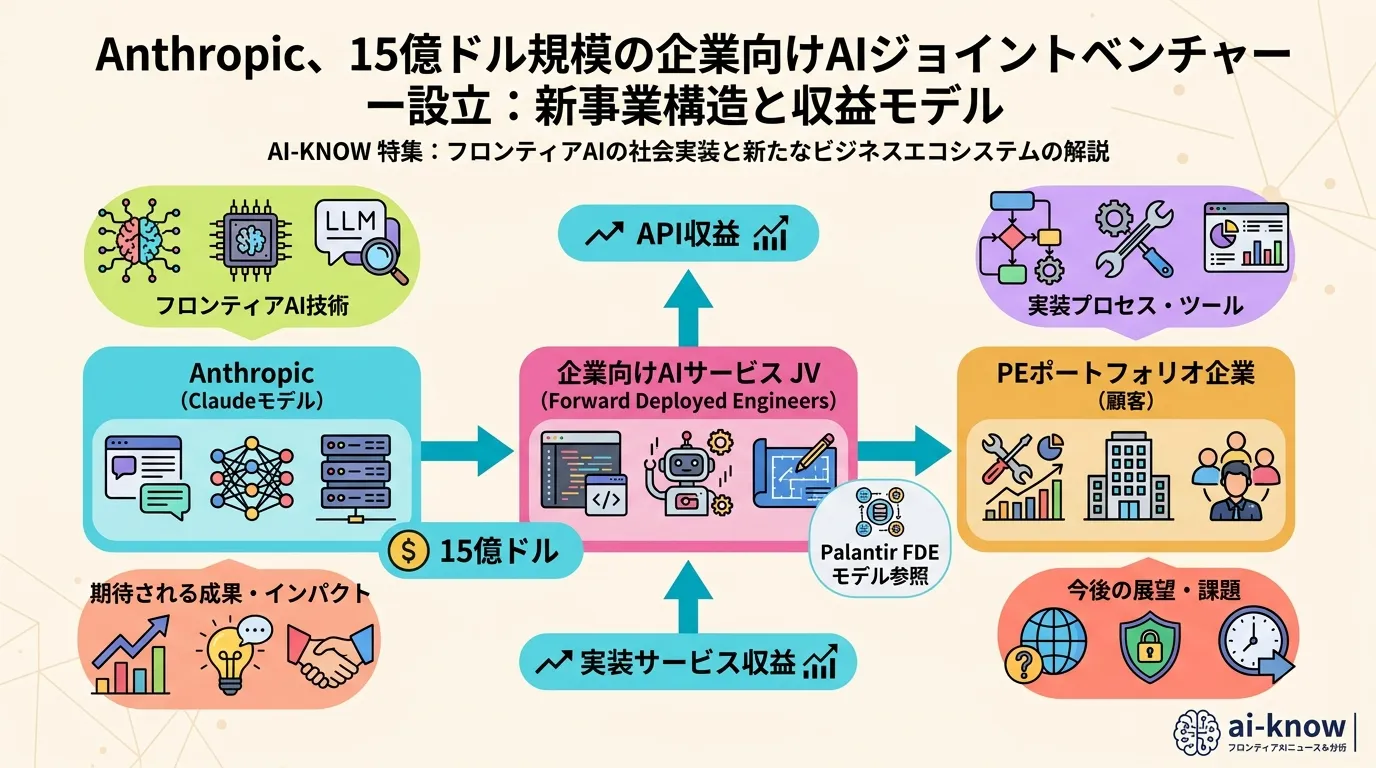

Anthropic has formed a new enterprise AI services company capitalized at approximately $1.5 billion, with Blackstone, Hellman & Friedman, and Goldman Sachs as lead investors. The roster also includes General Atlantic, Leonard Green, Apollo Global Management, Singapore’s GIC, and Sequoia Capital. The joint venture is structured not as a technology licensing arrangement but as a full-stack Enterprise AI services firm — one that deploys Anthropic engineers directly into customer organizations to integrate Claude into core business operations.

The business model is a deliberate echo of Palantir’s Forward-Deployed Engineer playbook: the model maker shows up with implementation talent in hand, owning the outcome rather than just selling the software.

The Strategic Logic

Anthropic’s run-rate revenue has grown from roughly $9 billion annualized at the end of 2025 to over $30 billion by May 2026. That trajectory is driven primarily by API revenue — Claude subscriptions and API calls from developers and enterprises. But model API revenue has a structural ceiling: it scales with usage but competes on price and capability, and the frontier keeps moving.

AI Commercialization through service delivery is a different story. Professional services revenue is stickier, differentiated by trust and domain expertise, and commands margins that pure SaaS API products don’t. Consulting firms have long known this. McKinsey, BCG, Accenture, and Deloitte are all building “AI transformation” practices on top of models from Anthropic, OpenAI, and Google. The JV is Anthropic’s move to capture that layer directly.

The PE capital structure adds a second angle: Blackstone and its co-investors control portfolio companies numbering in the hundreds. Each of those is a potential customer for enterprise Claude deployment. The JV doesn’t need to win a competitive procurement — it can walk into portfolio companies with the implicit weight of existing investor relationships. This is a captive market dynamic that traditional consulting firms can’t replicate.

Forward Deployment: What It Actually Means

The term “forward-deployed engineer” was coined at Palantir, where software engineers were embedded at customer sites — sometimes for months — to build, configure, and integrate Palantir’s data platforms in ways that could not be done remotely or via documentation alone. This model is operationally expensive (high headcount, high travel costs, limited scalability) but produces deep customer lock-in and extremely high contract values.

Anthropic’s JV applies the same logic to Claude. Rather than selling API access and letting customers figure out integration, the JV will provide:

- Domain experts who understand both Claude’s capabilities and the customer’s business processes

- Custom integration engineering (connecting Claude to internal systems, data lakes, document workflows)

- Ongoing optimization and fine-tuning support

- Probably, some form of proprietary tooling built on top of the Claude API

This is qualitatively different from what an SI (system integrator) or consulting firm can offer, because the people doing the work are from the organization that built the underlying model. They have access to internal roadmaps, pre-release features, and direct escalation paths for model behavior issues.

The Competitive Race: OpenAI Is Close Behind

Reporting on the same day as the Anthropic JV announcement indicated that OpenAI is in active discussions with TPG and Bain Capital to form a similar joint venture. If that JV materializes, the pattern becomes clear: frontier AI labs are not content to be commodity infrastructure providers. They want to own the value chain from model to enterprise outcome.

This puts them in direct competition with:

- Big 4 consulting firms (Deloitte, PwC, KPMG, EY) — which are growing AI practices built on vendor models

- Strategy consultancies (McKinsey, BCG) — which are selling AI strategy and are now also doing implementation

- Global SIs (Accenture, IBM, Infosys, Wipro) — which have large “AI transformation” practices anchored to partnerships with model vendors

The structural threat for these organizations is real: if Anthropic can deliver better enterprise AI outcomes because it understands the model more deeply than any third-party implementer ever could, the value argument for intermediary consulting collapses.

What Changes for Enterprises

For enterprise buyers, the JV creates a new option they didn’t have before: contract directly with the model maker for end-to-end implementation, rather than assembling a consulting team that interfaces with an API vendor. The trade-offs:

Advantages of the JV model:

- Direct access to model expertise and roadmap

- Potentially faster time-to-value on integration

- Single accountable party for outcomes

- Built-in escalation path for model behavior edge cases

Disadvantages:

- Vendor lock-in to Claude’s ecosystem intensifies

- Less flexibility to benchmark against competing models mid-engagement

- Scaling the JV’s headcount will take time; early demand may exceed capacity

For now, the JV is likely to target large enterprise accounts where the implementation complexity and contract value justify the forward-deployment cost structure.

Japan and Asia-Pacific Context

Japan’s enterprise AI adoption has been accelerating, driven by major corporations seeking productivity gains in a tight labor market. The consulting-led model has been dominant, with Accenture Japan, IBM Japan, and domestic SIs like NTT Data and Fujitsu running AI implementation projects. A Palantir/JV-style entry from a frontier AI lab would represent a significant structural disruption to that market.

Whether Anthropic’s JV expands into Japan directly — or whether a regional analog emerges — will be worth watching. The PE investors’ portfolio exposure in Japan and APAC (GIC alone has significant regional presence) creates a natural pipeline.

Related Articles

Anthropic and OpenAI Race to Form Enterprise AI Joint Ventures

Anthropic Launches Claude for Small Business: 15 Agentic Workflows to Close the SMB AI Gap

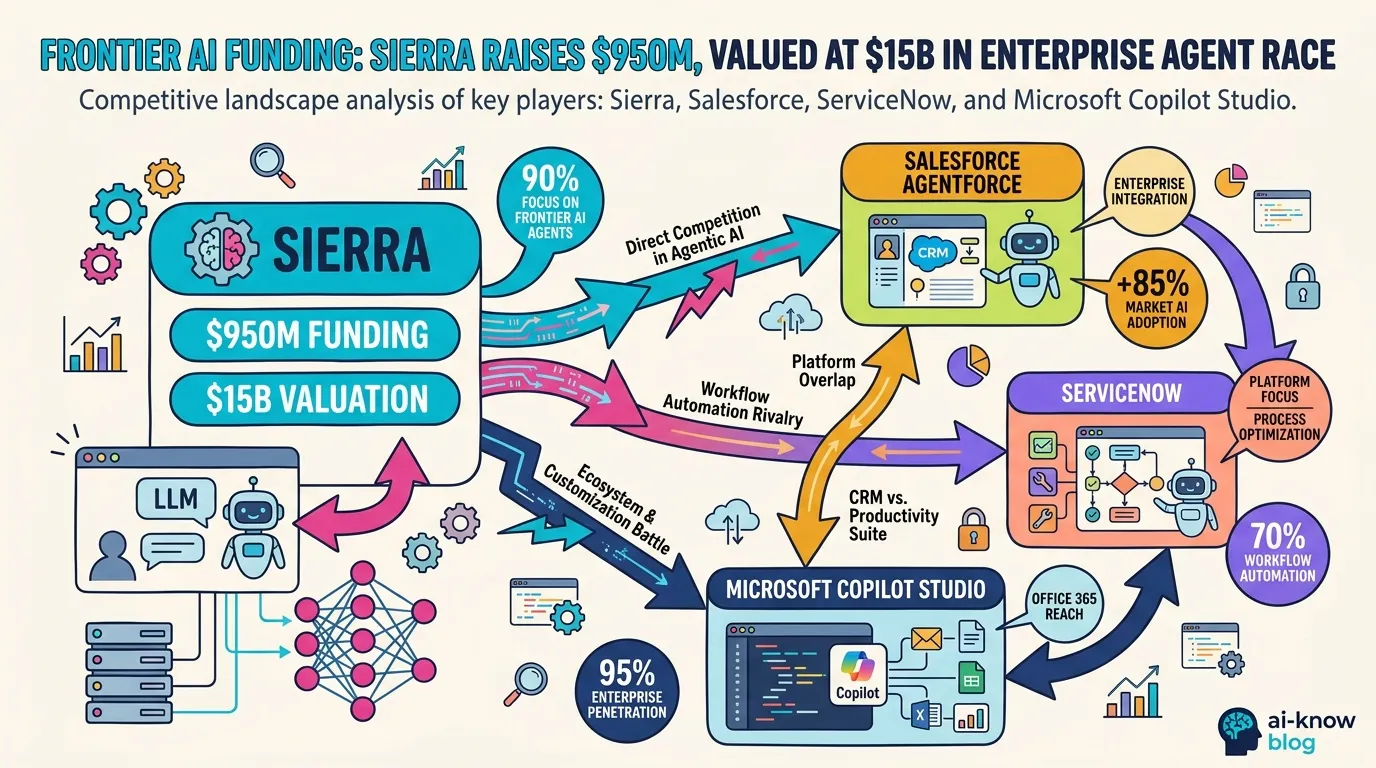

Sierra's $950M Raise Signals the Enterprise AI Consolidation War

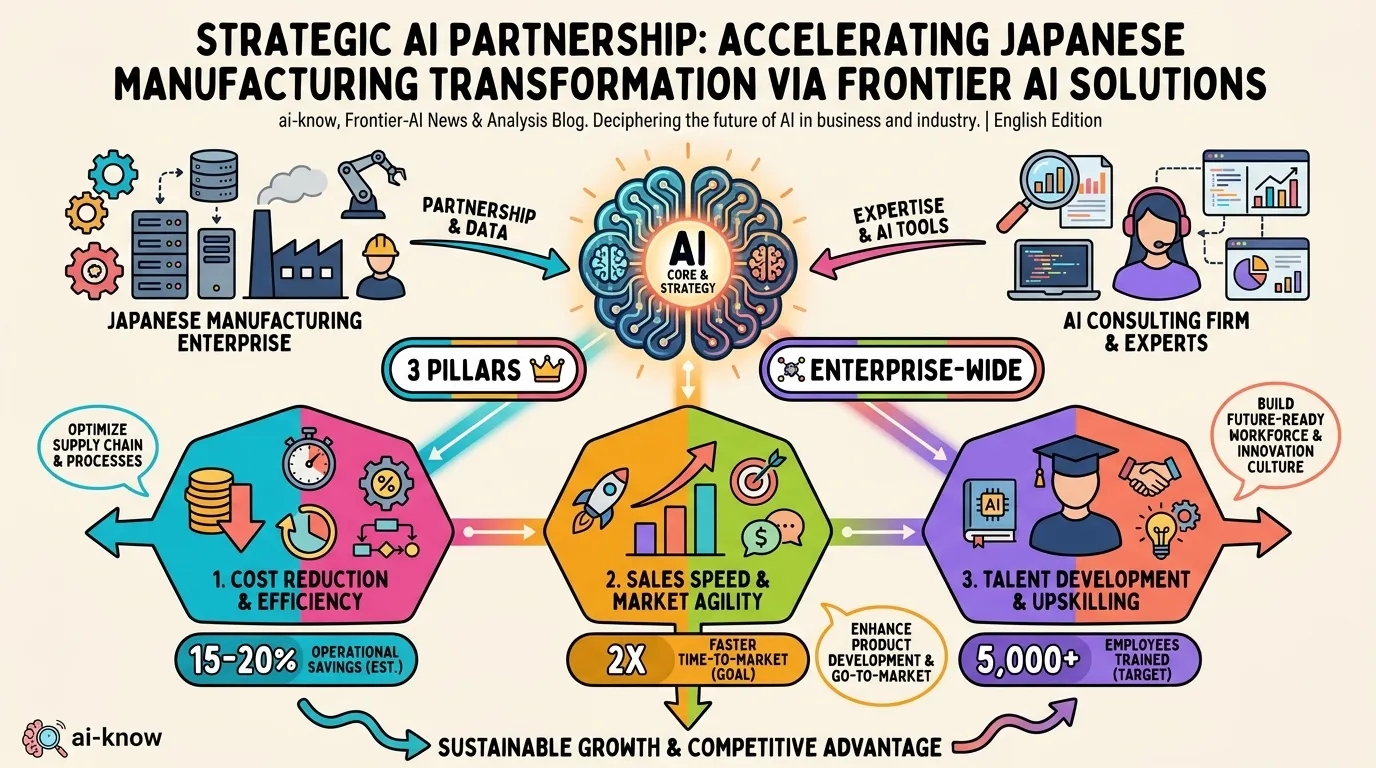

Accenture × NSK: AI-Driven Business Reinvention Moves to Full Scale in Japanese Manufacturing

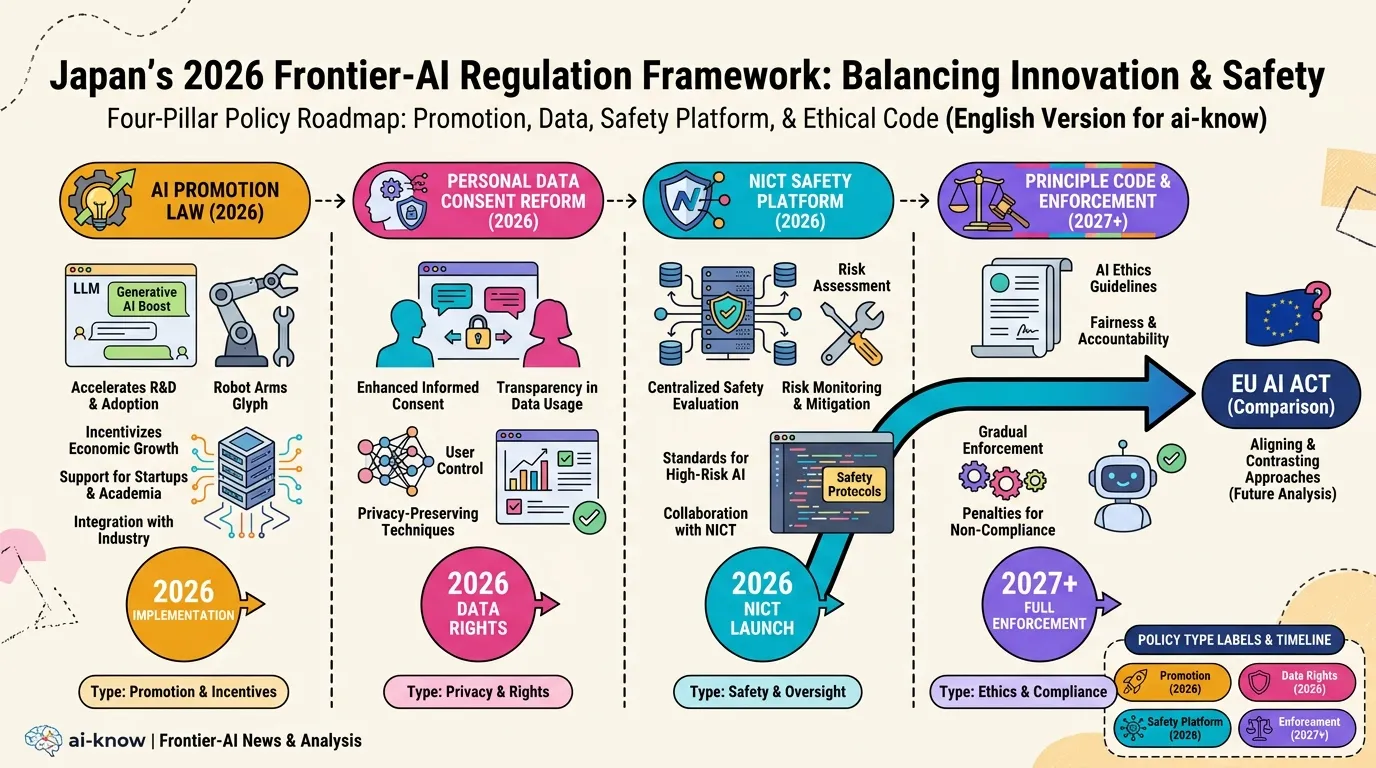

Japan AI Policy 2026: Promotion Law, Data Consent Reform, and the NICT Safety Platform